AI in credit scoring is no longer a futuristic idea—it’s rapidly becoming the gold standard in lending. Traditional credit models are outdated, biased, and slow. Lenders need faster, more accurate ways to assess risk. Borrowers need fairer, more inclusive access to credit. AI is delivering on both.

The Problem: Credit Scoring Is Failing the Modern Borrower

Conventional systems like FICO rely on rigid formulas and limited data. If you’re a freelancer, student, immigrant, or don’t have decades of credit history, you’re likely to be overlooked—even if you’re financially responsible.

Legacy models also:

- Penalize thin credit files

- Ignore real-time income or spending behavior

- Are vulnerable to bias and discrimination

For lenders, these limitations lead to inaccurate risk assessments, higher defaults, and lost business. For borrowers, it means unnecessary rejections and delays.

The Agitation: High Stakes, Growing Pressure

With loan defaults on the rise and regulatory focus increasing, banks and lenders are under pressure to improve both accuracy and fairness in credit decisions. Financial institutions that stick with outdated scoring tools face:

- Rising credit risk exposure

- Lower profit margins

- Compliance challenges with fairness and transparency laws

Lenders need a smarter, scalable solution—and fast.

The Solution: AI in Credit Scoring

AI in credit scoring applies machine learning to evaluate thousands of variables in real time. It goes far beyond the traditional credit report to analyze patterns in behavior, income streams, spending habits, and more. The result: more accurate, fair, and instant loan decisions.

Let’s explore the key benefits of integrating AI into credit scoring models.

1. Real-Time AI Loan Approval

AI automates what used to take days. Loan decisions are now made in seconds with high precision. By analyzing dynamic data, AI models can instantly flag potential defaults or approve trustworthy applicants—even if they lack a traditional credit history.

Use case: Fintech firms like Upstart and Zest AI are delivering real-time credit decisions with AI, increasing approvals while maintaining or lowering risk.

2. More Accurate Credit Risk Assessment

With machine learning credit risk models, lenders no longer rely on static rules. AI dynamically weighs variables like:

- Transaction frequency

- Cash flow volatility

- Employment and education history

- Online and mobile banking behavior

This means fewer bad loans and more accurate risk-adjusted pricing.

3. Fairer Lending Decisions

AI reduces human bias—when built responsibly. It ignores protected attributes (like race or gender) and focuses on behavioral data. This levels the playing field for applicants who would otherwise be rejected by legacy models.

Result: More inclusive access to credit for underserved groups such as gig workers and recent immigrants.

4. Adaptive Scoring with Live Data

Traditional scores are updated monthly at best. AI models update in real time. When a borrower’s financial situation changes—new job, large deposit, reduced expenses—their score can reflect that immediately.

This dynamic scoring makes lending decisions more relevant and timely.

5. Streamlined Lending Operations

AI doesn’t just score—it automates. It pulls documents, verifies identity, flags inconsistencies, and routes high-risk cases for human review. This reduces manual work, operational costs, and fraud.

Stat: Lenders using AI tools report up to 40% operational savings by automating decision workflows.

6. Better Fraud Prevention

AI is also a powerful defense against identity fraud and synthetic applications. It can detect anomalies in digital footprints, document inconsistencies, and suspicious behavioral patterns.

Want to learn how AI stops banking fraud? Read this detailed post:

👉 AI Fraud Detection in Banking

7. Regulatory-Ready Explainability

AI models used in credit scoring must meet regulatory expectations for transparency. Modern AI tools include explainability features that help institutions disclose why a decision was made—without exposing sensitive algorithmic data.

This satisfies legal requirements and builds consumer trust.

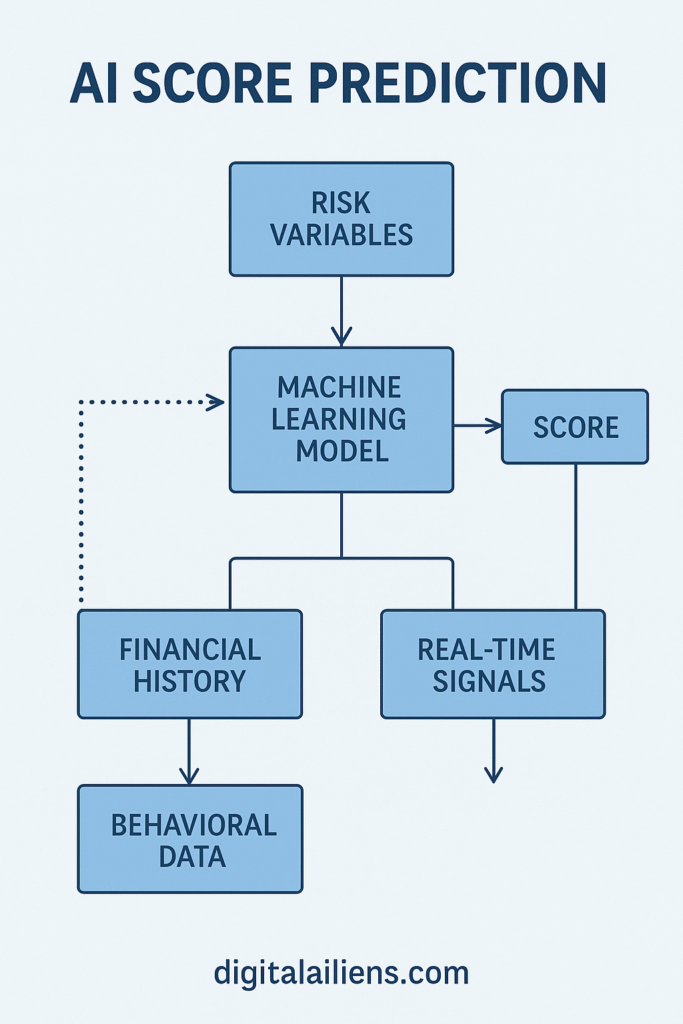

Visual: AI Score Prediction Workflow

Alt Text: Flowchart showing how machine learning processes financial history, behavioral data, and real-time signals to produce a credit score, with watermark digitalailiens.com.

Caption:

A visual overview of how AI models evaluate credit risk using diverse data inputs to generate fast, accurate, and fair credit scores. Image © digitalailiens.com.

The Bottom Line: Smarter Credit for a New Era

AI in credit scoring isn’t just a technology trend—it’s a transformation. It creates value for everyone involved:

- Borrowers get faster, fairer access to funds

- Lenders reduce defaults and operational waste

- Regulators gain better compliance visibility

And with every new data point, these models get smarter. Banks, fintechs, and credit bureaus embracing AI are setting new industry benchmarks.

Before wrapping up, it’s worth noting that leading institutions are already embracing this shift. For example, Experian has integrated AI to improve risk modeling and expand credit access, as detailed in various resources on their Advanced Analytics & Modeling page

and their AI-Driven Credit Risk Decisioning insights

. Meanwhile, FICO uses machine learning to enhance their scoring algorithms with greater precision and fairness, a topic they explore on their blog, such as in “Evolving Landscape of Machine Learning Relative to the FICO® Score” (FICO Blog Link

) and in their whitepaper “Algorithmic Credit Scoring and FICO’s Role in Developing Accurate, Unbiased, and Fair Credit Scoring Models” (FICO Whitepaper Link

). Reports by McKinsey confirm that AI-driven models can reduce default rates and operational costs significantly when deployed responsibly, a point highlighted in their “Building the AI bank of the future” report (McKinsey Report Link (PDF)

) and further elaborated in their insights on AI-powered decision making for banks. As adoption grows, AI in credit scoring is quickly becoming the new standard for forward-looking financial institutions.

What’s Next?

If you’re in the lending business, now’s the time to adopt AI credit scoring. Whether you’re building from scratch or integrating a vendor solution, ensure your model is transparent, ethical, and continuously updated.

Have a story or insight about AI in credit scoring? Share it in the comments.

Want more on AI in finance? Subscribe or explore more articles on DigitalAiliens.com.

FAQ: AI in Credit Scoring

1. What is AI in credit scoring and how does it work?

AI in credit scoring uses machine learning algorithms to assess an individual’s creditworthiness by analyzing both traditional (e.g., payment history) and alternative data (e.g., cash flow, employment trends, spending behavior). Unlike traditional scoring, AI models update dynamically and adapt to new patterns.

2. How is AI credit scoring different from traditional methods like FICO?

Traditional credit scores are based on fixed criteria and formulas. AI credit scoring models, however, process thousands of variables in real time and evolve over time, resulting in faster, more personalized, and potentially fairer credit decisions.

3. Can AI in credit scoring reduce bias and discrimination?

Yes, when designed responsibly. AI models can be trained to ignore protected attributes like race, gender, or age. By focusing on behavioral and transactional data, AI can help reduce human bias and support more inclusive lending practices.

4. What data does AI use to evaluate credit risk?

AI models analyze a mix of structured and unstructured data, including credit history, banking behavior, income consistency, payment timing, social signals (in some cases), and even device usage. This leads to a more comprehensive risk profile.

5. Is AI credit scoring legal and compliant with regulations?

Yes, but it must follow regulations like the Equal Credit Opportunity Act (ECOA), GDPR, and CCPA. Lenders must ensure their AI systems offer explainability, transparency, and non-discrimination, which many modern AI credit platforms now support.

6. Can AI help approve loans faster?

Absolutely. AI credit scoring enables real-time or near-instant loan approvals by automating credit analysis and decision-making. Fintechs and banks using AI often cut approval times from days to minutes.

7. Is AI credit scoring only used by fintech startups?

Not at all. While fintechs like Upstart or Zest AI were early adopters, traditional banks, credit unions, and even major bureaus like Experian and FICO are now integrating AI into their credit risk models.

8. Does AI scoring work for people with no credit history?

Yes. One of AI’s biggest strengths is handling “thin-file” borrowers by analyzing alternative data. This gives more people access to credit who would be invisible to traditional scoring systems.

9. How secure is the data used in AI credit scoring?

AI credit scoring platforms follow strict data privacy and security standards. They use encryption, anonymization, and access controls to protect sensitive borrower information, often exceeding regulatory requirements.

10. Can I dispute a loan decision made by AI?

Yes. Lenders are required to provide reasons for credit denial, even with AI systems. Modern AI platforms include explainability tools, so you can understand what factors influenced the decision and challenge any inaccuracies.